Relations of Extraction:

Taxation and Women’s Citizenship in the Maritimes, 1914-1955

Shirley TillotsonDalhousie University

Abstract

This article considers four different ways in which gender relations figured in tax matters and their connection to citizenship between 1914 and the mid-1950s. Topics covered include interventions in tax debates, tax evasion in working-class work, taxation and women’s voting rights, and women’s response to the introduction of mass income tax in 1942. The general conclusion that follows from these narratives is that gender norms and the diverse organization of families were implicated in the relations of extraction (i.e., the complex web of connections between taxation practices and the various rights and obligations of citizenship).Résumé

Cet article examine quatre façons dont les rapports hommes-femmes apparaissent dans les questions fiscales et leur lien avec la citoyenneté entre 1914 et le milieu des années 1950. Les sujets traités comprennent les interventions dans les débats fiscaux, l’évasion fiscale dans le travail ouvrier, la taxation et le droit de vote des femmes, et la réponse des femmes à l’introduction généralisée de l’impôt sur le revenu en 1942. La conclusion générale qui découle de l’exposé de ces faits est que les normes sexuelles et l’organisation diverse des familles avaient une incidence dans les relations d’extraction (c.-à-d., le réseau complexe de liens entre les pratiques fiscales et les divers droits et obligations de la citoyenneté).1 TO DO THINGS SUCCESSFULLY AS A GROUP, people must contribute from their own resources part of what is needed for the group’s common projects. Making those contributions is a core part of being a citizen, as important to citizenship as is the right to share in the benefits of common projects or the right to be treated equally by the group and by the state that, more or less, carries out the group’s will.1 As women fought for citizen rights in the modern West, one point at issue was what counted as the sort of contribution that warranted the status of citizen. Was bearing arms the essential contribution of a citizen, or should bearing and rearing children count as women’s contribution to the state? Did the taxes that widows or spinsters paid earn them a voice in public spending, or should even those women be excluded from choosing their representatives in public life?2 As the women’s suffrage movement began to score its major victories in the early 20th century, there was a loosening of the 19th century’s tight connections between citizen rights and gendered perceptions of citizen contribution. But those connections had been complex and dense. Their remaking in the 20th century entailed many changes, not just the enacting of one statute in the national legislature. Women’s political disabilities had been premised on the limits of their scope as economic actors and on the norms of family relationships, which in turn shaped the contributions they could reasonably be expected to make. Remaking political citizenship thus meant reorganizing the expectations of women’s contributions to family, to economic life, and to the state. An important, and too little understood, place where these expectations and therefore citizenship was remade was in the tax regime – the “relations of extraction” as Martin Daunton has called this set of policies, practices, and politics.3

2 This article considers several aspects of these relations of extraction in the Maritimes between 1910 and 1955. During this period, many Canadian women began to explore and make use of their new civil rights as voters. They found themselves in a polity that was remaking its mechanisms of contribution and reconsidering the role of taxpaying in the franchise. In this same period, there was also underway significant change in the history of Confederation as a system of resource sharing, with the federal government asking Canadians for more tax dollars and the Maritime region fighting hard to extract from the national community more money to support its expanding social services and economic infrastructure. In what follows, I explore the relationships among these three currents in early 20th century politics and society: 1) changes in womanhood as a citizenship category; 2) the impact of changes in federal tax policy and practices; and, to a lesser degree, 3) the campaign for Maritime Rights within Confederation. There is evidence in the tax history of this period that the continuing influence on tax law of separate spheres ideology was holding Maritime women back from full citizenship. But in this reconnaissance of tax history I will also show that women in the Maritimes participated exactly as did other Canadian women in many of the tax policy controversies of this period. During this period, I will also suggest, the means by which women could be heard opened up, as the politician-dominated discussion of the region’s taxable capacity and its rights in Confederation was jostled aside by experts in economics and by the democratic exigencies of war finance. By engaging in the nation-wide debates about the obligations of citizenship, Maritime women helped to advance the project of defining women socially, economically, and politically as rights-bearing individuals, equal with men as democratic citizens.

3 I have framed my exploration around four aspects of the tax history of this period: the debate about new taxes after the First World War, some types of tax evasion in the interwar years, the changing relation of taxpaying and the civic franchise throughout the period, and the gendered reaction to the mass-based federal income tax that was introduced in 1942. Each of these aspects of taxation affected very immediately housewives of all classes, and women of all marital statuses in small businesses and in the families of wage earners, farmers, fishers, and the salaried middle-class. In each of these categories, an analysis that considers the intersection of taxation with the gendered relations of work and family suggests that tax policy has been both made and experienced in gendered, and sometimes regionally specific, ways.

4 Although I have attempted to make the survey presented here widely inclusive, it is nevertheless only a limited sample of possibly relevant tax topics. I have left aside taxation of natural resources, corporate income, and taxation forms such as gasoline taxes. These seemed either to repeat themes I cover already in other ways, or to open up further, unmanageably large areas of discussion. There are also limits in geographic scope. While I touch on some rural history topics, the emphasis is primarily urban. And in my treatment of municipal taxation I focus on Saint John, whose tax history I have discussed in more detail elsewhere.4 Finally, I have emphasized the common constraints that Confederation set upon governments everywhere in the Maritime provinces, and to keep this essay to a manageable length have only hinted at the region’s diversity. Even with its many limits, this article covers a large territory and therefore remains quite general. I intend only to open up tax history, particularly in its gendered aspects, as a subject for further research. There is much room for historians to work in this field, as much remains to be done concerning the effects of specific local tax regimes, the openings these tax regimes made possible for women’s political engagements and economic agency, and the limitations that the regimes imposed.

The debate over new taxes, 1918-1926: Ella Murray, suffragist and tax pundit

5 Through a kind of historical accident, a Halifax woman came to occupy a prominent place in the history of women and taxation in 20th-century Canada. Journalist and suffragist Ella M. Murray spent some of her formative years in the United States during a period of suffrage and tax reform ferment, and came back to Canada having been marked by the experience. The daughter of a Halifax temperance activist, Murray had been opposed to women’s suffrage as a young woman in the 1870s. But she had joined the cause during the ten years that she spent in Boston in the 1890s, and between 1905 and 1913 she had lived in modern America’s feminist heartland – New York City. There, she had joined delegations to the state capitol to petition for the vote, and “walked in the first great Woman suffrage parade in the early spring of 1913.”5 These American experiences may help to explain why taxation was her issue of choice in the early 1920s. American suffragists had used the Revolutionary War’s rhetoric of “no taxation without representation” as a set piece of their arguments.6 And in American political life, the federal income tax had been a major issue from the 1890s through to 1913. A 1909 constitutional amendment to allow a federal tax was followed by a four-year ratification fight, a process that made participating in taxation debate a staple of politics during Murray’s New York years.7 So it is not altogether surprising that Ella Murray should have found the tax questions of wartime and post-war Canada to be “absorbingly interesting.”8 That a Nova Scotian woman would have spent some of her young adult life in the United States was fairly common, and one of the normal ways in which Maritimers brought American influences into Canada.9

6 Drawing on her American experiences, Murray made it her mission to induce the National Council of Women (NCW) of Canada to share her passion about taxation. “Until women understand taxation,” she asserted, “they are not in a position to undertake public life.”10 Beginning in 1918, shortly after her return to Halifax and continuing until 1927 (when she once again left the city), Ella Murray was the convener of the taxation committee both in the Halifax Local Council of Women and at the national level.11 From those platforms she delivered both general education on tax theory and specific policy proposals, with both general justice and gender justice in mind. Murray’s work on tax questions in the National Council of Women covered all of the topical tax issues of the day.12

7 Her guide in tax analysis was that mainstay of the international liberal tradition since the 18th century – Adam Smith’s The Wealth of Nations. Murray drew on Smith’s four principles of taxation as quoted by John Stuart Mill in his Principles of Political Economy, and in her reports to the National Council of Women conventions Murray repeatedly offered a digested version of these principles.13 Like others before her and since, she referred to the “four canons of taxation” as though they were eternal absolutes. At the same time, and seemingly for contingent historical reasons, she exercised some strategic selectiveness in her reporting of them. In Smith’s original conceptualization, the features of a good tax are as follows: 1) its amount is proportional to the taxpayer’s ability to pay; 2) its amount is certain and not arbitrary, so as to prevent discretionary judgment by the collector (and therefore to prevent occasions for corrupt dealings); 3) the timing or method of collection of the tax payment should be convenient, so as to prevent even a tax of a reasonable amount falling due on some occasion when it was particularly hard to pay; and 4) the means of collecting it should be as economical as possible, to help ensure that the tax levels remain as low as possible. Murray’s summary reflected this canon through a Millian lens, emphasizing his interpretation of “ability to pay” as meaning “equality of sacrifice” or equal treatment before the law. Murray’s ordinary language version of Mill’s “equality of sacrifice” standard was that a good tax “should give none an advantage and place none at a disadvantage as compared with any others.” Unlike Mill, however, she did not acknowledge that this was an unattainable “standard of perfection.”14 More notably, Murray’s summary of Smith completely omitted Smith’s third standard of good taxation (convenience); she subdivided Smith’s fourth principle to make up for missing number three. Some particulars of national tax politics in the 1910s and 1920s and the pocketbook politics of organized womanhood explain why Murray selected as she did.15

8 Within national tax politics, Ella Murray supported a particular policy option – one that located her within the broad current of progressive reform. Her particular ambition was to promote a new means of raising revenue, so she wanted there to be a national tax on land.16 This was the policy of a reform organization called the Canadian League for Taxation of Land Values (CLTLV), an organization that advanced at the national level the ideals of the municipally and provincially oriented Single Tax Association.17 The new league was formed in 1916, specifically to advocate a federal tax on land values as a means of paying off the national war debt. In partisan terms, land tax enthusiasts tended to be Liberals, United Farmers, or (later) Progressives. Not surprisingly, Nellie McClung was a member.18 While enthusiasm for the single tax is well-known as a feature of the western-dominated Progressive party, the Maritimes had its own single-taxers. The Nova Scotian representatives in the CLTLV, numbering 13, were, along with Manitoba, second in number only to the large list of Ontarian members. And one of the four New Brunswick representatives, F.L. (Frank) Potts, had been elected to the Saint John Board of Commissioners in 1914 after having campaigned as a single-taxer. No marginal figure, Potts was elected twice to the New Brunswick legislative assembly (in 1917 and 1925) and in 1924-26 served as Saint John’s mayor.19 All this is to say that Ella Murray was active in one of the main tax reform projects of the day, one that was part of the Maritime region’s political culture.

9 Her association with this tax reform project explains why she (and others of this political bent) omitted part of the standard Smithian principles. One of Smith’s two examples of a “convenient” tax was a type of consumption tax – the luxury tax. A luxury tax is “convenient” in Smith’s sense because the consumer chooses when to buy a taxed item, and thus when to pay the tax. Consumption taxes, whether on necessities or luxuries, were also convenient by Smithian standards because they parcelled out tax payments in small increments, making payment as painless as possible. But single-taxers, with their emphasis on direct taxation of land values, disputed the value of painlessness in taxation. They preferred that people know what taxes they are paying, so that taxpayers would be vigilant about governments’ taxing and spending. Income tax advocates also held this view.20 It was a staple criticism of consumption taxes. From this point of view, conveniently arranged taxes were of doubtful merit because convenience allowed a government to raise tax levels stealthily, outside the range of taxpayer awareness. Single-taxers also pointed out that consumption taxes had nothing to do with the ability to pay, extracting as they did pennies from the poor rather than collecting on the unearned surplus of the owners of land. The heightened consumer prices that free traders attributed to the tariff were, in fact, the result of the sort of “convenient” taxes to which the Progressives and their fellow travellers in the single-tax movement objected. For Ella Murray, speaking to an audience of women whose interests were very much those of the domestic pocketbook, “conveniency” seemed not at all consistent with tax fairness – or conducive to thrift.21 Her deference to Adam Smith stopped short of endorsing consumption taxes.

10 From this logic, Murray opposed two taxes that federal Finance Minister Sir Henry Drayton introduced in 1920 for the first time at the federal level – a luxury tax and a sales tax. In her view, not only were these taxes regressive and covert, but the luxury tax also came couched in a rhetoric that made no sense to her. Drayton’s 1920 budget rhetoric emphasized two objectives: 1) to launch the huge enterprise of paying off Canada’s war debts, and 2) to help lower the cost of living by fighting inflation. The luxury tax was meant both to raise revenue and, by reducing consumer demand, to lower overall price levels. In Drayton’s discussion of inflation, he argued that “every individual whose circumstances permit it” should help lower the cost of living by “reducing expenditure whenever possible.” When he introduced the tax on luxury spending, he reiterated its dual purpose:Not only is more revenue necessary but extravagant and luxurious expenditure ought to be checked. Just so long as expenditure on non-essentials and extravagant expenditure continues, just so much longer will the drop in the value of essentials be postponed. On those having income more than necessary for properly maintaining themselves and families, there rests a special duty of saving whenever possible and in this manner adding to the available financial resources for development and for industrial undertakings. Extravagant buying should stop.22All of this was sound economics; in theory, at least, the general level of prices falls when the general level of effective demand declines.

11 But the list of luxuries in Drayton’s budget speech made his rhetoric inflammatory. No one disputed that opera cloaks and gold dinner services were luxuries. Other items on his legislated list of luxuries were, however, more controversial.23 The issues arose around items such as $10 boots and $18 blouses. As one Saint John merchant, Robert Macaulay, explained to Drayton in the 1920 public hearings on federal taxation that followed Drayton’s budget: “The customer doesn’t object to paying $19.80 for the [shirt]waist until she is shown that $1.80 of the price is for luxury tax.” Her objection, Macaulay went on to say, was to the “paternalism” implied by the tax: “We can buy cigarettes at 18 cents a package, and we all know perfectly well that that includes 7 cents tax, but we are perfectly willing to pay it. If, however, the government should say in a paternal way, ‘we believe it is criminal and extravagant to smoke cigarettes, and therefore we tax every packet of cigarettes 7 cents,’ you would resent it.”24 It seems likely that many women felt, as Ella Murray asserted, that the “so called luxury tax” was not borne only by those “who indulge in extravagant, luxurious things,” but that it was charged against purchases that were necessities to “the great middle class.”25 Drayton’s argument that pinching pennies even harder would, by “reducing demand,” lead to lower prices did not, apparently, outweigh the offense Murray took at the implication that middle-class housewives were “extravagant” and should cut back their spending. Macroeconomic price theory was too remote from commonsense to register in Murray’s analysis of the luxury or sales taxes. Her critique centred, as one might reasonably expect, on the high cost of living and emphasized the way that luxury taxes and sales taxes could strain the household budgets of the middle class. Murray’s outrage at the luxury tax was shared by many consumers, merchants, and manufacturers. In response to this widespread protest, within a few weeks of the finance minister’s return from his cross-country taxation consultations in the fall of 1920, the federal government repealed the luxury tax on 18 December.26

12 The federal government’s concession to popular opposition must have been sweet to Murray, who held that citizenship entailed protesting against injustice and insisted that women’s enfranchisement at the dominion level now allowed them the means to challenge unjust taxes. Women’s moral authority, embodied in a non-partisan critique of injustice, was for Murray a defining element of women’s citizenship. In her 1926 report to the National Council of Women on tax matters, she insisted “IT MUST BE POSSIBLE TO EXPRESS JUSTICE IN ALL THE ESSENTIAL RELATIONS OF MAN TO MAN. THE TASK BEFORE US IS TO DISCOVER HOW.” In the context of that year’s federal election, however, tax policy had become too much a partisan issue for the deliberately non-partisan organization. Murray refrained from presenting a specific resolution on tax policy in 1926 because any resolution would “have a political complexion.”27 But the reality of post-suffrage politics had made nonpartisanship increasingly an untenable position. As economist and journalist B.K. Sandwell told the Empire Club in 1928, when he was making his own effort to speak as a non-partisan: “Unfortunately, budgets in Canada are an excessively political topic. They are almost the only political topic.”28 Taxation policy was thus, for maternal feminism, difficult territory to travel.29

13 By 1926, Murray’s preferred federal tax, the land-value tax, had lost its place on the policy agenda. Member of Parliament W.C. Good, on behalf of the Progressives, had championed it vigorously in the House of Commons, but because it duplicated many provincial and municipal land taxes, and because it required a national standard in land-value assessment, it faced insurmountable administrative problems. The Liberals and Conservatives simply refused to take it seriously.30 The land-value tax had had enormous moral appeal, something that suited a woman of principle such as Ella Murray. She regarded all other taxes as failing to meet her adapted version of the Smithian standard of fairness. For a time (after 1926), she left both Halifax and her role as the NCW’s tax pundit. However, others, both nationally and in the Maritimes, took up this role vigorously. In Moncton, author Aida Boyer McAnn took an important leadership role on women’s economic and tax issues during the 1930s both within her community and nationally within the NCW.31 In the 1950s, Isabel Finlayson (née Grant), a Nova Scotian graduate of Dalhousie University, also played an important role in raising women’s tax issues. Living in Ottawa, she spearheaded an assault – independent of the NCW – on the federal tax code’s treatment of married women.32 While the study of taxation was often a tough sell within the NCW movement, Ella Murray’s passion helped to inspire other women in the Maritimes and Canada to claim their voice as tax critics.

Working-class women and tax evasion in the interwar years

14 Ella Murray’s work on tax expressed two features of her class. First, she had particularly emphasized the impact of the luxury tax on middle-class women’s management of the family budget. Like Nellie McClung, she spoke out on taxation in 1920 (and later) in part because of the threats such taxes posed to middle-class consumption: McClung had described the post-war taxes as making of salaried and middle-class people “the new poor.”33 Second, speaking in policy forums and agitating for political action, Murray engaged in tax politics in a way that expressed her middle-class occupation as a journalist. Tax talk was her business. But taxation touched working-class women as well, affecting their working lives and family budgets in class-specific ways. In particular, tax evasion arose as a strategy for survival among some of the region’s labouring women as they struggled to get by.

15 In the case of the luxury tax, the women who served as sale clerks and cashiers in the region’s clothing stores experienced it not as taxpayers but as tax collectors. After the 1920 budget was passed, these women found themselves having to memorize new lists of taxable and non-taxable goods, and varying rates of tax, so as to inform their customers accurately about prices. While the finance minister allowed that he did not himself know what a camisole was – never mind how it should be classified for tax purposes – was a silk camisole underwear (and therefore not taxable) or was it a taxable luxury item (because it was silk)? Saint John merchant Robert Macaulay complained: “Our girls are not trained as excise collectors. They are qualified to sell merchandise, and the more enthusiastic they may be to fulfill their ordinary work, the more likely they are to fail in [tax collecting].” As Macaulay tactfully explained: “Our most enthusiastic sales people are more apt to overlook the tax than some of the slower and less enthusiastic ones.”34 “Overlooking” the tax would no doubt have helped to make a sale, while remembering to charge the tax might lead to bad feelings and maybe to the loss of the sale. In short, these sales clerks found themselves facing either the unpleasant task of enforcing the luxury tax or anxiety-inducing pressure from customers to collaborate in evading it.35

16 Complicating the sales clerk’s job was the fact that some of the women customers (and, we might suspect, some of the men, too) found the tax calculations seemingly arbitrary. Macaulay observed: “A great many women who have perhaps gone through 8 or 9 grades in school in a superficial way, quite cultivated and refined ladies, have forgotten their mathematics, and the clerks have to explain to them the percentage. You will be surprised at the number of really clever people who are at sea on a question of percentage.” The sales clerk had to thus become an arithmetic teacher as well as having to engage in discussions about what constituted a luxury. The frustrations associated with collecting the luxury tax were further compounded when excise stamps in various denominations were issued as an administrative convenience. Inconveniently, however, if a store ran out of some necessary denomination of the stamps late on a Saturday afternoon, the sales requiring that amount of luxury tax could not legally be completed, and the customer had to be asked to return on Monday morning. Imagine the temptation for both clerk and customer to “overlook” the tax. Countering that temptation was the risk that the revenue officials would lay charges against the shop owner in magistrate’s court, or the likelihood that rumours would begin that certain clerks or certain shops would “give you a break” late on Saturday (and the legal problems that this could potentially cause). Inconsistencies in the charging of these taxes – “Is this a scarf (taxable) or a muffler (not taxable)?” – could compromise the “the honour and reputation” of a merchant. This tax thus made clerks and cashiers subject to their employer’s anxious surveillance.36 In short, women retail workers in the better stores could not have been fans of the luxury tax. Both the risk of inadvertently failing to collect it and the temptation to collude with their customers in evading it complicated their jobs.

17 Later on, in the mid-1920s, working-class women’s lives were also touched by a different tax evasion issue that stirred up another enormous political storm. That issue was corruption in the federal Department of Customs and Excise. Ineffectual efforts to improve customs collection that had begun early in the 1920s were overtaken in 1925 by an aggressive partisan exposure of massive commercial smuggling. Cars, luxury fashions, silk, diamonds, and liquor were being brought into the country, with the collusion of Canadian customs officials, by means calculated to evade import duties, excises, and sales taxes. The investigation of the customs scandal of 1926, known in its day as the smuggling inquiry, revealed dramatically what many Canadians no doubt already knew – that coastal and border communities were the sites of major, and ineffectually policed, tax evasion. The problem was not private individuals sneaking a few things for their own use across the border; this longstanding practice in popular culture fell below the radar of the investigating committee and the subsequent judicial commission. Rather, the investigation targeted the ways in which some of Canada’s distilleries, breweries, car dealers, jewellers, and fashion retailers were competing unfairly with honest businesses and, in the process, defrauding the public treasury. In addition, the Department of External Affairs was worried about the international tensions generated by some Canadians’ collusion in undermining prohibition in the United States.37

18 To the extent that Maritime suffragists were also themselves prohibitionists, politically active women such as Local Council of Women members no doubt rejoiced when the smuggling inquiry investigated the booze traffic as a major source of corruption in the Maritimes’ customs administration.38 But many other Maritimers would have winked at some kinds of smuggling. Excepting in manufacturing towns, free trade sentiment was widespread.39 Ella Murray was certainly of this stripe: her NCW reports had pointed to the harmful impact on both producers and consumers in western Canada and the Maritimes of the protective tariff tax.40 She was not alone in observing that customs collection enabled corruption and that excise taxes were expensive to collect.41 Acadians told a folk tale about Ti-Jean and the taxman that scorchingly stigmatized customs collectors as the wielders of absurd and arbitrary authority.42 Moonshining and homebrewing were also forms of tax evasion. Assessing PEI’s revenue sources in 1945, tax expert J.L. Lattimer noted how low PEI’s collections on liquor taxes were in comparison with those of the other two Maritime provinces and dryly observed: “This lack of revenue is not due to the location. It must be something else. The best way to avoid taxation on any commodity is to produce and consume it directly.”43 Prohibitionists or not, Maritimers had various reasons to suspect and dislike the customs and excise tax system.

19 For some Maritime women, though, customs and excise taxes had a rather different meaning. These taxes presented business opportunities for the economically desperate. Poor women surviving at the margins of the economy used excise tax evasion – bootlegging – as a means of getting a living. There were two ways of doing this. One was to actually run booze across the border. I have found only one account of a woman who engaged in this kind of high-end, relatively profitable bootlegging, the kind that produced the legendary cops and robbers narratives of popular prohibition history. This account, by Clifford Rose recalling his days as a temperance inspector in Pictou County in the late 1920s, described Amy Mason, the “Queen of the Bootleggers,” as a glamorous, adventuresome beauty. But her choice of a life of profitable crime, he claims, was simply the result of there having been no other way for her to earn a living as a single woman in 1920s Pictou County. And the other women in Rose’s accounts, running small “rum dives,” sometimes with a prostitution sideline, were recognizably simply desperate women without better options. Three sisters, orphaned in their teens, became “the sport of men’s lust”; two of them ran a “bugbeer joint” in New Glasgow, while the youngest had been adopted out. Another pair of sisters operated a beer and brothel outfit that was tolerated because, were they to be jailed, their fatherless children would have to be sent to the overseers of the poor and supported on the poor rates. Desperate as these single women were, a married woman might be almost as badly off. “Delores N.,” who described herself as “98 pounds of hell,” had a husband. But he was an (unspecified) “war casualty” and a mean drunk. When Rose had to shut down Delores’s operation temporarily, she asked Rose angrily how he expected she was going to eat. For these women, tax evasion was simply a survival strategy – a (largely tolerated) crime of desperation.44 Seen from this perspective, there is little in the history of bootlegging to warrant the “boy’s own adventure story” tone that swathes in a certain glamour the popular history of excise tax evasion during the 1920s.

20 Viewing the rum trade from the point of view of the rum-runners’ wives is another standpoint from which we can see the troubles entailed in surviving from the profits of tax evasion. The risks of the trade to their husbands’ life and liberty were considerable, even though “fishing for rum” was widely accepted on the Atlantic coast as a normal, even respectable way to earn a living. Both its respectability and its risks for fishermen’s families can be seen in a letter to the editor by a Mahone Bay crew member, injured at work on a rum-running schooner. He complained that he was not eligible for workmen’s compensation, and he asked if someone could inform him “if the crews of rum running schooners have not as much right to compensation from the board as anyone else.” And he also spoke in defense of the compensation rights of the widows of men killed on the job (presumably even those men who had been shot by U.S. revenue agents). Unless rum-runners had been making their employer’s contributions for their crew payroll, their widows were unlikely ever to have received pensions. Moreover, rum-runners faced real risks of prosecution for infringements of the Customs and Excise Act, risks that carried potential harm to their wives. In 1923, journalist Edwin Smith wrote about Nova Scotia fishing captains who, facing debt and difficulties in the fishery, tried to make a bit of easy money smuggling liquor from Saint-Pierre to the South Shore. His tales emphasized the fallings out and betrayals among rum-runners, with previously honest captains losing their schooners and their livelihood and, sometimes, serving substantial prison terms. Summarizing his moral, Smith concluded that the results of smuggling could be “disastrous” not only for the captain, but for his wife and family.45 In the mid-1920s, attempts to crack down on smuggling raised the risk of such consequences. In 1925, a new clause in the Customs and Excise Act allowed a convicted rum-runner to be imprisoned on what had previously been a lesser offence. This took the community of Devil’s Island, at the approaches of Halifax Harbour, by surprise. One of their own, Allen Henneberry, was sentenced to two years in the penitentiary, leaving without a breadwinner his six young children and aged mother, who were “solely dependent upon him for their existence.” Devil’s Islanders organized a petition among residents of Halifax and Dartmouth, asking that Henneberry’s sentence be commuted. His family responsibilities featured in the petition.46 Quite aside from the lack of workmen’s compensation coverage, rum-running carried particular risks for the bold adventurer’s family.

21 For a time, to be sure, rum-running could give a drinker and brawler like the famous Teddy Kirk the chance to become a solid breadwinner. Raised in hard circumstances in PEI, Kirk had turned to rum-running in 1922. Jobs in regular shipping were hard to come by; he had just married and needed to support his new wife, Maude. The young couple lived with Maude’s mother, a widow, divorcee, or perhaps an unmarried mother who in 1919 had been one of the first to rent a row house in Halifax’s new Hydrostone neighbourhood. In November 1925, Captain Teddy took over the lease, but during the following three-and-a-half years during which he was responsible for paying the rent, it was paid up for at most six months. Perhaps his fame (and possibly gifts from his cargoes to the rent collecting agent) gave his wife an advantage in her relationship with her landlord, the Halifax Relief Commission. Other tenants who fell behind in their rent for as little as three months had some of their property seized and were evicted or moved out in under a year. No such proceedings were taken against Teddy Kirk. Eventually, though, Maude Kirk’s secondhand luck ran out, and in June 1929 she, by now with young children, was forced to leave the Hydrostones and move to the city’s old North End slums. By the next year, 1930, Captain Teddy, sporting a “massive drinker’s belly” was captaining ships that no one else would take – ones that were hardly seaworthy. In 1931, he disappeared at sea, apparently, at age 40, the victim of a shipwreck. Maude Kirk then moved a few blocks away to live with a married couple (perhaps her sister and her brother-in-law). She was likely left with little or nothing but a family to support and memories of a brief marriage.47 Being a rum-runner’s wife was not to be a wife like any other. However “normal” Teddy Kirk’s enterprise had been, it put Maude at more than the usual risk of losing her husband, either to misadventure or to prison. As the customs and excise law and enforcement practices came to be more aggressive in the 1920s and 1930s, these risks to the wives who lived by the rum runners’ earnings only increased.

22 In relation to various forms of federal taxation in the interwar years, then, women in the Maritimes as consumers, as collectors, as tax evaders, and as wives of tax evaders responded to new taxes and new forms of enforcement. For Ella Murray, and others like her, engaging in policy debate about taxation expressed the new citizenship rights that had been granted to some women at the federal level. For Maude Kirk, and others like her, the tax regime appeared (as perhaps it always had) mainly as a means for acquiring illicit earnings or as a cause of police raids and criminal prosecutions.

Paying the price of citizenship: taxpaying and municipal suffrage, 1914-1955

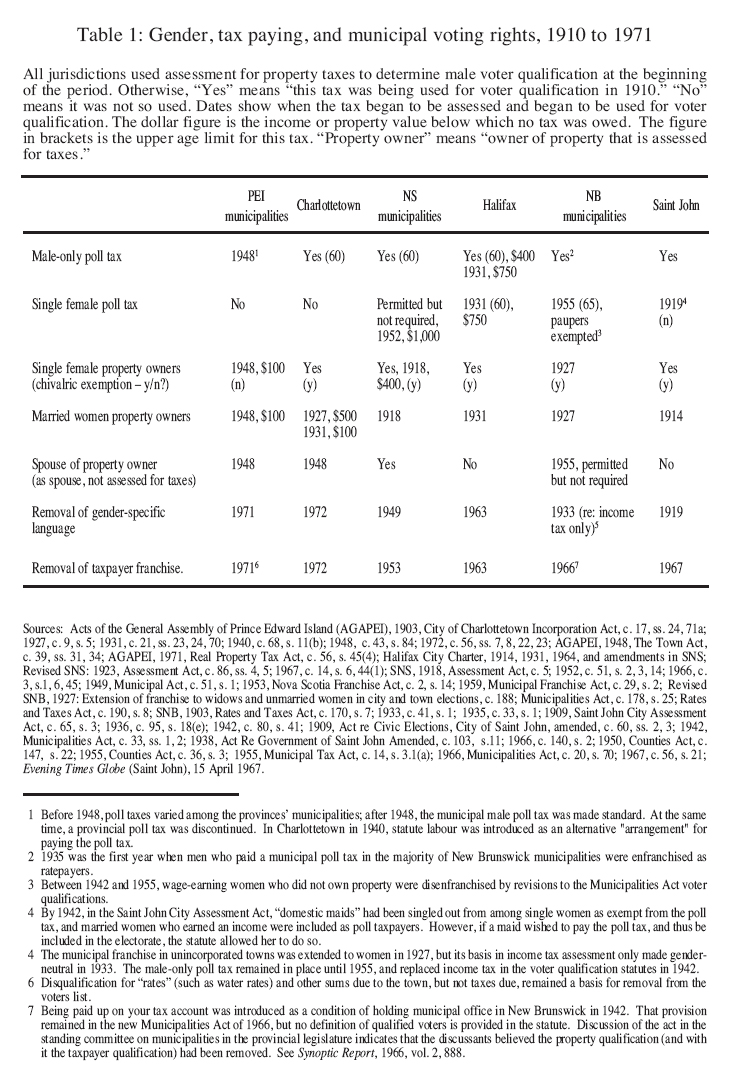

23 Citizenship rights, tax obligations, and survival were linked very directly in another aspect of taxation: municipal taxes. Until the 1950s or 1960s, in most Maritime municipalities – as in many American towns and cities – taxpaying and voting rights were directly connected in that the franchise was a taxpayer franchise (see Table 1).48 That is to say, the right to vote was based on whether the voter had paid his or her taxes. The taxpayer franchise was linked to the property franchise if all municipal taxes were property taxes. But when the franchise was truly a taxpayer franchise, it was not simply the ownership of property that conveyed voting rights. Head taxes, more commonly known as poll taxes, could be levied on the propertyless; paying those taxes also served, in a taxpayer-franchise municipality, as qualification to vote. When a taxpayer’s finances were tight, as they were for many in the 1930s, the link between taxation and the franchise could mean people found themselves forced to choose between, on the one hand, paying their tax bill and voting or, on the other, not paying it and eating.

24 The dire choices of the 1930s took place during a period when women’s municipal voting rights and tax obligations were changing. Unevenly, but steadily, Maritime women’s municipal voting rights grew while at the same time, between 1914 and the mid-1950s, their tax obligations expanded (see Table 1). For example, at the beginning of this period (in 1914) Halifax allowed single and widowed women to vote if they had been assessed for taxes; only if they appeared on the property tax assessment roll would they appear on the voters’ list.49 However, for men – married or not – there was a mechanism to ensure that they could vote even if they had little or no assessable property: so long as an otherwise eligible male voter had an income of $400 or more, he was obliged to pay a $4 poll tax. And the names on the list of poll taxpayers were added to the voters’ list.50 Exemption from the poll tax thus disenfranchised the poorest residents of Halifax, men and women alike, and probably disproportionately African Nova Scotian men. But only single women wage-earners (or those living on a small trickle of investment income) were absolutely denied a place on the voters’ list if they were propertyless. And in this city no married woman, even among the middle class, could vote at all in civic elections. In 1920, the Halifax Council of Women sought to make married women eligible to vote by having Halifax’s “household tax” (10 per cent of the real property tax) assessed in the name of “the partner who is not assessed on real estate, whether it be the husband or the wife.”51 This proposal was unsuccessful; it was not until the abolition of the taxpayer franchise in Halifax’s 1963 charter revision that married women had full municipal voting rights. Although in 1949 the province had legislated a sex-inclusive franchise for Nova Scotia’s municipalities, the provincial Franchise Act, which determined the municipal voters’ list, was amended in 1953 to allow for the disenfranchisement of non-taxpayers and relief recipients and even exclusion by marital status.52 Thus, the extension of the municipal franchise to women was limited by their place in the tax regime.

25 In Saint John, by contrast to Halifax, the 1914 civic election saw the passage of a proposition to allow married women who were property owners the right to vote, thus joining propertied single and widowed women as voters. An even larger step towards women’s enfranchisement was taken in 1919, when Saint John’s Civic Elections Act was revised to make tax arrears, whether owed by men or women, a disqualification for voting. While attempting to increase pressure to pay taxes, this statute also removed any remaining sex disqualification on municipal voting.53 Single and widowed women began thereafter to be assessed for the poll tax.54 In the smaller municipalities of the province, the municipal vote was extended later and more gradually. A 1927 provincial statute enfranchised single women and widows in city and town elections, but it was not until 1933 that the Rates and Taxes Act, which governed tax assessment outside the chartered cities, removed the qualifier “male” from its description of the owners of taxable income.55 So, again, an apparently gender-neutral franchise became completely so when the tax assessment statute, to which voter qualification was linked, was made gender-neutral.

Table 1: Gender, tax paying, and municipal voting rights, 1910 to 1971

Display large image of Table 1

26 Saint John, while leading the way in the enfranchisement of women municipally, had a tax regime that was exigent to the point of injustice. For example, there was no statutory exemption by income level from the poll tax obligation until 1942, even for the poorest (including some of those collecting relief). In theory, then, Saint John’s broad-based tax requirements made the city’s franchise highly democratic, making taxpayers of all and making every taxpayer potentially a voter. However, the longstanding record of low-income taxpayers failing to pay even the poll tax, and thus failing to qualify for the vote, should make us sceptical about the democratic intentions of the city’s policy-makers. Indeed, when in 1909 and 1918 New Brunswick legislators were contemplating tax exemptions for the poorest of Saint John men, the objection that won the day and justified an increased male poll tax was that if poor men were allowed to vote without paying taxes the city would be governed by those whose “interests” in the city were insignificant. Participants in this debate also alluded to the fact that the level of other taxes was determined by the amount of revenue supposed to be generated by the poll tax. All other things being equal, if more money was collected in poll taxes then property owners’ tax bills would be lower.56 To reassure the payers of property taxes that their rates were as low as possible, then, the city had to be seen to be collecting poll taxes aggressively and in earnest.

27 The enormous variety and detail of municipal enfranchisement and taxation statutes deserves further investigation in order to test for reliable generalizations about its underlying consistencies. But on the grounds of my research so far, I think it safe to venture that tax liability was, in the interwar years, typically determined in part by sex and that where the municipal franchise was a taxpayer franchise, women’s voting rights could not be extended without their tax obligations also being increased.

28 As public revenues suffered in the 1930s, the extension of greater rights and responsibilities to women was notable in New Brunswick, and not only in the 1933 redefinition of taxable income mentioned above. In 1936, a proposed extension of the Moncton poll tax to women provoked comments in the provincial legislature that tellingly indicate the cultural meanings attached to such changes. The proposal covered both married and single women, exempting only those whose income was under $600, the same exemption threshold as for men. The mayor of Moncton, speaking on the bill in the legislature’s municipalities committee, pointed to wage-earning women as an untapped revenue source: “Many girls and women earned as much as men and some females earned more. Some married women earned as much as their husbands.” And he pointed out that, in return for this new tax obligation, the bill granted women “additional privileges”: in the same year, women in Moncton became eligible to run for mayor or aldermen and to vote if they were assessed for taxes.57

29 In the combination of new tax obligations and enhanced political rights, we should recognize the effect of the modern liberal perspective that sees women as full citizens if they are “like men” – i.e., economic actors in the market. Against that perspective, the MLA from Westmorland opposed the proposal on principled grounds drawn from an older, separate spheres logic. He “objected to getting into a channel of asking the weaker sex to assume the burden of financing the town.” He proposed raising the income exemption to $1,000 (suggesting his view that women workers likely earned less than that amount). The mayor, in reply, repudiated this chivalric view, and insisted that he was simply trying to “equalize the tax burden between women and men.” Again, he turned to the language of liberalism, using “equality of sacrifice” to legitimate this tax proposal.58

30 The chivalric view taken by his opponent was not merely an individual viewpoint. Special tax exemptions for widows and spinsters were commonly built into municipal tax statutes, on the assumption that such women were likely to be poor through no remediable fault of their own. Similarly, special tax exemptions for male householders reflected the assumption that men and not women were obliged to support dependants and thus would have less surplus income available to be taxed. In these ways, the Saint John assessment statute in 1918 was typical of the way municipal tax law more generally reflected the values and assumptions of 19th-century familial and citizenship regimes.

31 The robust tradition of women’s and feminist political activism at the municipal level began to change this dimension of the local state relatively slowly, it seems, in the decades after enfranchisement and the extension of tax obligations at the federal level. For instance, in 1926, Saint John’s municipal income tax was revised to allow that women householders might be entitled to claim the breadwinner exemption based on their support for dependants.59 This latter measure helped to reduce female breadwinners’ tax burden, on the basis of a liberal egalitarian rather than a chivalric, welfarist logic. As it was modified to conform to egalitarian principles, the assessment act was moving toward suffrage-era universalism and male taxpayer privilege was being removed. As well, in the 1930s, the single female wage earner’s obligation to pay the price of citizenship, the poll tax, was being exacted with the same firmness as the men’s, married or single. But the tax statute and its enforcement continued to have sex-specific elements of special treatment for poorer widows and self-supporting single women.

32 These welfarist elements in Saint John’s municipal tax regime reflected the fact that local taxes could genuinely be a burden on the poor. I have examined a broad sample of the records of the Saint John city council’s Appeals Committee and Board of Revision from the 1880s to the 1930s.60 These records provide many examples of how annual tax bills of as little as $6 or $7 dollars could lead to threatening visits from the city marshall, whose job it was to collect these debts. Before 1918, the granting of appeals for relief from taxes was largely discretionary. As I have shown in some detail elsewhere, Saint John’s councillors in the pre-suffrage era were more willing to relieve women than men from all of their taxes.61 In a sample of 132 appeals in 1910 for relief on grounds of inability to pay, 30.3 per cent of the appellants (counting both male and female) were relieved of all arrears. But of the eleven women in that sample, nine (81.8 per cent of the female appellants) were granted full relief. Men were usually expected to pay at least their poll tax, on the basis of which they could vote. Women did not yet have either that tax obligation or that civil right, and so the councillors did not hold them to even a minimal standard of citizenship obligation.

33 Tax appeal records from 1935 suggest that a chivalric, welfarist logic continued to dominate in the treatment of women’s linked rights and obligations as taxpayers, even in the post-suffrage era. Comparing the results of appeals by widows and spinsters in 1935 to those in 1910, we can see the same chivalric bias, partly based in the continuing presence in the law of a “female” exemption and partly in continuing discretionary enforcement, based on the assumption of women’s more restricted economic options.

34 The cases of widows and spinsters who were assessed for real estate taxes show how close to the bone these women lived. They found themselves asking for tax relief because the unemployment crisis had deprived them of the rental income from their properties. In working-class neighbourhoods, rents tended to be $10 to $15 a month, usually from one or two tenants in flats or rooms in the subdivided houses where these widows or single women lived. When the tenants were paying, this meant a typical annual revenue, if the landlady had two tenants, of $240 to $360 a year. This was often her only income. The “female” exemption from property tax on $5,000 of assessed value enjoyed by the widows and spinsters was worth $200 as a reduction of tax payable, enough to keep in the landlady’s hands a substantial proportion of the small income that she derived from owning a modest property.62 Even if this exemption left her owing taxes (and some of these widow and spinster appellants did owe amounts ranging from $85 to $125), most were afforded some further relief, either by the board accepting partial payment in place of the full amount owing, or at least by the board recommending that the case “be not pressed” or that the notice of sale be cancelled. It was not difficult, apparently, for the board to accept the assertions, recorded in several of these cases, that the rental income from these inherited properties was the women owners’ only means and that reduction or loss of that income during the unemployment crisis made them simply unable to pay taxes.63

35 These female owners of real estate enjoyed their municipal franchise as payers of tax related to property. Unlike female wage earners, they were not assessed a poll tax. When, in the face of massive tax default during the depths of the Depression, the local state considered severing temporarily the link between property taxpaying and voting rights, the voting rights of this group of women property owners were ignored. Labour leader James Whitebone challenged the city’s 1933 proposal to allow property owners to vote regardless of having unpaid taxes on their account. He rightly pointed out that the measure still required non-property owners to pay their poll tax every year in order to vote and that the city’s proposal was therefore a repugnant class measure.64 But Whitebone entirely disregarded the interest in citizenship held by those women whose only tax obligation (and therefore their only claim to a place on the voters’ list) was based in small property ownership. Nor did the city council’s appeals committee care much about women property owners’ voting rights. When they decided, chivalrously, to allow some women to be relieved of all taxes or to be “not pressed” to pay the ones they owed, the city fathers were again, as they had before the suffrage victories of the ’teens, implying that these women’s voting rights were dispensable.

36 At the municipal level, then, women’s voting rights had begun to be extended in the interwar years. But at the municipal level, even more strongly than at the provincial or national level, the state was understood as a kind of corporation, where paying taxes was the equivalent of a membership fee, a service fee, or a stock price.65 Only by paying taxes did one acquire a vote in the affairs of the corporation. So long as women were distinctively exempted from tax obligations, because of their distinctively limited economic agency, they had no vote, and so therefore a limited voice in the business of the town. While Ella Murray was rejoicing in women’s increased voice in national politics, women’s right to political voice at the municipal level was still in a murky and muddled state. The expansion of women’s taxpaying met with chivalric objections and concessions, but the need for a larger revenue base for municipalities was clear and that need to increase taxable capacity helped to underpin the gradual removal of women’s twinned exemption from municipal responsibilities and their exclusion from municipal voting rights.

Remaking the tax regime: politics and democracy, 1920-1949

37 Removing women’s tax exemptions at the municipal level was hardly going to solve the problem of raising adequate revenue that the Maritime provinces faced in the interwar years. Nonetheless, the small steps toward collecting the female poll tax and including women’s wages in New Brunswick’s definition of taxable income were symbolic of the larger project that governments at all level were engaged in during the interwar years: remaking the tax regime so that revenue matched spending responsibilities. To understand what kind of voice women had in tax questions, it is important to recognize that the process of making of tax policy was changing. In the interwar years, the making of tax policy was dominated by partisan and regional politics. But frustrations were building in many quarters and, in response, two other styles of policy-making were about to take on new importance. One was a technical liberalism, forcefully articulated during the 1930s. It offered little by way of an opening to women’s participation, except in so far as a few women were economists, accountants, and tax lawyers. The other, a democratic style, emerged during the war. It was more open to popular opinion, and thus to a diversity of women’s voices.

38 The years from 1920 to 1937 saw more-or-less constant negotiating between the provincial governments in the Maritimes and the dominion government about taxes and subsidies. The view of dominion officials was that the Maritime provinces had created their own problems by unwise expenditure or were failing to tax at a reasonable level. These provinces, as became well known over the course of the Maritime Rights movement, were reluctant to impose higher taxes since they regarded higher dominion subsidies as their due. The question of taxable capacity became highly politicized, both in partisan and regional ways, in the course of these stalemated federal-provincial discussions. To address this stalemate and other apparently intractable issues in the nation’s tax “system,” a royal commission on taxation was promised and, in 1937, the commission, entitled the Royal Commission on Dominion-Provincial Relations – popularly known as the Rowell-Sirois Commission – began its investigation.66

39 The promise of the Rowell-Sirois Commission was that experts could fix what politicians had fouled up.67 With proper research, the state could know who could pay what kinds of taxes, and the determination of taxable capacity would no longer be a matter of opinion or relative political power among regions or parties. The commission’s description of the country’s taxation practices was as blistering as Ella Murray’s had been, but for a different reason. While she had excoriated the lack of principle in tax policy, the Rowell-Sirois report blamed a lack of expertise. In the view of the commissioners, the main injustices of taxation in Canada were the result of revenue policy that had been made (by politicians) on the basis of short-term expedience rather than on sound tax theory: “It would be hard,” the commissioners concluded, “to apply any canon to the intricate mass of taxation which exists in Canada today.” Worse still, the investigation of tax incidence was at so rudimentary a level of development in Canada that “it is . . . impossible to say with confidence what weight of taxation any one taxpayer bears.”68

40 The meaning of this observation for democracy was clear, if unfortunate: the commissioners concluded that “the ultimate consequences of taxation may be so obscure that it is quite futile to rely on the taxpayers themselves making known through their parliamentary representatives the full effects of the tax.”69 The political stalemate, in their view, was the result of inadequate research. Neither individual citizens nor politicians had the ability to know the effects of tax policy; only special experts, with skills in scientific data-gathering about recondite phenomena such as the multiplier effect, could judge the effects of taxation. On the basis of this analysis, the Rowell-Sirois report proposed that a cadre of social science experts should undertake tax reform. The voice of the people, and women’s voices in particular (judging from the condescending treatment accorded women witnesses at the Rowell-Sirois hearings), had little to do with their thinking on tax policy.70

41 Then the war hit. Regionalist arguments were sidelined (though not silenced). In 1941, the federal government temporarily took control of income taxes, both municipal and provincial, across the country and, in July 1942, federal Finance Minister (and Kentville, Nova Scotia, lawyer) J.L. Ilsley proposed in his budget speech Canada’s first national, mass-based income tax. For the first time, the Canadian government would require all but the very poorest of its citizens to pay a direct tax on their income. The bartering and badgering of fiscal federalism was, for the war’s duration, no longer central to tax policy. Instead, the multitude of new taxpayers focused the federal government’s interest on the voice of ordinary citizens. Collecting income tax in any era requires a high level of voluntary compliance, if collecting and enforcement are not to be prohibitively expensive. The mass income tax therefore sharpened Ilsley’s ear in listening to the voices of the people.

42 Ilsley and his tax advisors guessed that, somewhere out there among the masses, there were enough small sums collectible via an income tax to make a difference in the enormous and daunting task of financing the war. And, indeed, personal income tax collections grew to be the single largest revenue source other than borrowing during the war years. The 1942 collections were over five times what the pre-war income tax had produced, and by the end of the war the federal personal income tax yielded seven times more, as a percentage of GDP, than had that tax in 1939 (its best pre-war year).71 Broadening the base (as well as raising the rates) had indeed shown that there was unused taxable capacity in Canada. Women formed a significant part of that untapped pool of prospective taxpayers: more than ever before, their small pay packets and modest retirement incomes or widow’s pensions came within the reach of the taxman. In this kind of policy environment, the voices of housewives and ordinary working women had weight.

43 The tax contributions required by the 1942 income tax stretched many Canadians’ household budgets to what they felt was the breaking point. And because of this strain, many taxpayers looked closely at the exemptions and thresholds in the tax statute to see if the burden was indeed being distributed fairly and imposed realistically. In the correspondence files of the finance minister, his senior officials, and other federal politicians, there is a host of letters written in July 1942 and afterwards to inform the nation’s leaders of problems with the new personal income tax. Among the writers of those letters, women raised particular concerns. Two of the most commonly reiterated had to do with the problems that the new tax regime represented for widows and other single women and also for married women workers. Two examples from the Maritimes will illustrate the impact on these women of the 1942 war income tax. They wrote, not to express regional grievances, but to explain their own personal hardships.

44 One letter came from Mrs. Augusta Gertrude Griffin of Woodstock, New Brunswick. Mrs. Griffin’s letter to Ilsley, signed A.G. Griffin and written shortly after Ilsley delivered his war tax budget in July 1942, is remarkable for its depth, its literacy, and its combination of affecting personal detail and sharp sociological analysis.72 Its author, born in 1881, was from one of Woodstock’s leading business and political families: her father, H.A. Connell, had been the town’s mayor during her youth. As a young woman she had travelled the world; likely, she took a university degree at the turn of the century. It is easy to imagine her as having been a New Woman, even though she was born and raised in a rural New Brunswick town, far from centres of cultural ferment like Greenwich Village. She married relatively late, at 33, becoming in 1914 the second wife of a widowed, 40-year-old American physician, Dr. Thomas W. Griffin. She also became a stepmother to two teenaged girls and, 19 years later, Dr. Griffin’s widow. In 1942, when she wrote to Ilsley, she introduced herself as speaking for older single women living in “the lower [income] brackets.” Though she owned a substantial house, her income may well have been, as she claimed, modest. Her husband had been a popular doctor in Woodstock for 30 years, but small town doctors were often far from wealthy.73

45 Augusta Griffin had two points to make about Ilsley’s 1942 budget. She asked that single women homeowners be allowed the same amount of tax exemption as were married men and that investment income derived from an estate (the widow’s basic income) be allowed the same level of exemption as wage or salary income. These points hardly seem the material for an emotionally charged text, yet Mrs. Griffin made them so. Depicting herself as struggling to stay off the “charity rolls” or government support, she argued that the tax exemptions she asked for would help “we lone women over 50” to “maintain the one thing left them, their independence. For that, no matter how we carry on, is all that is left us, but our memories.”74

46 She made her case for the first point – that single women as homeowners should be able to claim a married exemption – by arguing first for the value of homeowning to the community. The homeowning widow paid property taxes and employed labour to maintain her home. Second, she pointed to the ways in which war conditions had combined with the normal challenges of widowhood to make the expenses of homeowning similar to the expenses of maintaining a dependent wife. In the absence of a husband, the older single woman had to pay wages to have her firewood chopped, coal shovelled into her furnace, storm windows installed, and home repairs done. The wartime labour market meant that she had now to pay higher wages for this help. Third, both her house and the investments on which a (middle class) widow lived were the results of thrift, which saved government the cost of supporting widows who would otherwise be dependent. Allowing some of her income to be exempt (as some of earned income was) would enable her to survive on the basis of this thrift, rather than force her to ask for charity. Finally, she claimed that those who feared having to give up their homes in order to balance their budgets were the “smallest class” of taxpayers, so that exempting more of their income and thus collecting fewer tax dollars from them could have no appreciable effect on the war effort.75

47 A point that she did not make, but which might well have helped fire her indignation, was that until the 1932 tax year a widow had been able, in fact, to claim an equivalent-to-married exemption as a householder if in her home she employed a full-time servant. From 1932, entitlement to this exemption was narrowed, becoming claimable only by those widows and widowers whose home sheltered a dependant, not an employee. Still, for the federal income tax’s first 15 years, the statute recognized being a householder, whether married or not, as entitling the taxpayer to amounts ranging from $1,200 to $2,000 in exempt income, in addition to the basic individual exemption. Given housekeepers’ wages, three-quarters of that extra, untaxed income would have been available for homeownership expenses rather than spent on a housekeeper’s pay.76 Looking back, some might wonder why a sturdy 61-year-old should not have been expected to chop her own wood or shovel her own coal. Working-class widows of her community no doubt did much or all of such work themselves. But if we accept Mrs. Griffin’s assumption that doing this work herself was impossible, then it follows that owning a home on her own was genuinely like having a dependant whose support expenses were considerable.77

48 Concerning her point about investment income, Mrs. Griffin’s arguments pointed to problems that were also linked to her particular generational and gender experience. Before making her case about investment income, she first insisted that older women wanted to earn their living but were constrained by employers’ prejudices. “Trained women,” she asserted, were being “barred” from employment on the grounds of age. Other older women without specific training found that they could not compete with the “manual dexterity” of younger women. “We lone women who are over 50 who are able to work ask for it,” she concluded, before asking on behalf of those who could not work the tax exemptions that would enable them to keep their homes or to survive independently in rooming houses. Worth noting here are the limits of the wartime market for women’s labour; as Jennifer Stephen has pointed out, discrimination against older women was indeed a problem that employment experts sought to correct in the labour mobilization efforts of the Second World War.78 In 1942, the independent, twenty-something New Woman of 1910 found herself, now in her fifties, regarded as too old to be hirable. Independence, once a brave political stand, had become an elusive personal goal. Age combined with gender to limit economic options. But Augusta Griffin, a middle-aged, middle-class woman raised in late-Victorian, rural New Brunswick, nonetheless thought it reasonable to assume that single older women would indeed prefer to work rather than depend on relatives. “Many older people feel they should not live with their children except in cases of dire necessity,” she wrote. “They feel it is not fair to youth. They try to adapt themselves to the times.”79

49 To enable such women to keep their home, or at least to live “like a good sport” in a boarding house, Mrs. Griffin urged that the income war tax treat investment income in ways that acknowledged the fact that, under difficult conditions, her generation had provided for women’s old age through thrift. She pointed out that rising expenses that resulted from the wartime economy meant it was growing more difficult for some widows to get by on the income from their investments. The strain on widows’ resources was compounded by the fact that many had debts from the 1930s that now needed to be paid. Investment returns had also dropped. And, most importantly for Griffin’s point about taxation, income from annuities that had been designed to support a widow in her old age were now subject to a four per cent surtax on unearned income (albeit with $1,500 of such income exempt from the surtax, though not from the general tax). Moreover, as prices rose, workers’ purchasing power was preserved by cost-of-living bonuses while those living on investment income saw their margin of security shrink. And, as Griffin pointed out, tax policies targeted unearned income treated widows and older single women unfairly as rentier parasites. She argued that older women who were surviving on the property accumulated by husbands, fathers, or by their own “individual effort” were not simply dependants or privileged idlers, but were making contributions as mothers, householders, and community volunteers. The notion that their investment income was somehow less worthy of tax exemption than was wage or salary income seemed wrong to Augusta Griffin.80

50 It also seemed wrong to Edith Lang, the National Council of Women’s tax committee convener during the Second World War. In 1941, commenting on that year’s revisions to the Income War Tax Act, Lang remarked “the greatly extended tax on investment income,” which was “in principle, a fair tax,” should have continued to be structured so that “widows and people over 60” were exempted.81 Though Griffin had not been active in the NCW, it is not surprising that the issues she raised in her letter to Ilsley about tax exemptions for widow’s retirement funds were also expressed nationally by Lang and the NCW. Threats to the well-being of widows were threats to the viability of the breadwinner/housewife marriage, an institution that Canada’s maternal feminists stoutly supported. Only if women were provided for by husbands, post mortem as during the husband’s lifetime, would a housewife’s sacrifice of her economic independence during marriage be regarded as fair and practical. Criticism of how widows were treated in the federal tax regime thus remained a frequent theme in the NCW’s tax critiques from the late 1930s through to the final abolition of the Dominion Succession Duty Act in 1969.82 In the short term, critiques such as Mrs. Griffin made in 1942 were used in 1945 by a royal commission to justify tax breaks for widows’ annuities – measures that were quickly implemented.83 In the campaigns concerning the taxation of widows’ resources, women in the Maritimes played no distinctive role; but because the elderly as a percentage of the Maritime region’s population was already noticeably growing during the 1950s, the tax treatment of older women would have had specific practical meaning in the region.84

51 Just as widows across the country were worried about their personal income tax problems, so, too, were the tax increases faced by married working mothers a widespread preoccupation. Married women who were earning a wage doing war work featured prominently among the finance minister’s correspondents. Margaret Gillespie of West Saint John was typical in the complaint she raised, though her style of writing was unique. Mrs. Gillespie was a telegraph operator, and consequently was a woman of distinctively few words. Explaining her reasons for being employed, she wrote “personally feel should be working considering the great shortage of experienced telegraph operators at present time.” In 1941, she had gone back to her pre-war job as a telegrapher for the Canadian Pacific Railway (CPR). She had previously been at home, raising her young children, before she patriotically decided to help with the CPR’s shortage of operators (who were essential workers in the railway system). Now, she told Ilsley, her husband had to pay the wages of a “full time housekeeper” to care for their two children, aged six and twelve. She pointed out that she was being taxed 28 per cent of her earnings, which she felt was “excessive under circumstances and [made working] hardly worth the effort involved.” She also said that her being employed had increased her husband’s taxation. Ilsley was able to reply that, while her working had indeed increased her husband’s tax bill in 1941, the 1942 budget now allowed Mr. Gillespie to keep his married man’s exemption. Between them the couple would therefore have $360 more in tax exempt income than they had had in 1941, all of it applied to the calculation of her husband’s taxable income. Depending on what that did to Mr. Gillespie’s income bracket, having this additional income exempted would reduce his tax bill by $100 to $170 a year or about $15 a month.85 Nonetheless, however small the amount, and admitting that the higher rates of the 1942 budget meant that Mr. Gillespie would still be paying more than he had in 1939, Ilsley pointed out that the government had attempted to take into account the concerns of women in Mrs. Gillespie’s position.

52 With other women also writing to Ilsley in more aggressive terms about how much they resented having their newfound war-work wages taken as taxes (as well as paying for child care and housekeeping costs), it is easy to understand why tax policy was adjusted to help them cope. Even as a symbolic gesture, the special tax exemption seemed essential for recruiting and keeping married women in war work. But with the dollar value of the tax exemption not all that high, these women war workers must themselves have faced the harsh realities of wartime labour markets as they attempted to find housekeepers. In Nova Scotia, and probably elsewhere in the Maritimes, newspaper ads solicited women to move en masse to Ontario to work in war industries. A letter to the editor of the Halifax Chronicle protested that these ads reflected “the . . . centralization of war effort in Upper Canada,” which was leading to “the emigration of Nova Scotia’s woman power to what looks like green fields far away.”86 Working mothers looking for inexpensive child care in the Maritimes in these circumstances were caught between conflicting branches of the government’s employment policy, being invited to work and help with the war but also having to compete with war industries for female labour. In larger industrial centres in Ontario and Quebec, publicly funded child day care centres provided part of a solution; Mrs. Gillespie’s situation in Saint John suggests what was likely a more common, and probably more expensive, type of arrangement in the Maritimes.

53 Meanwhile, even the small concession that the Department of Finance made to help meet the challenges of combining patriotic war work and family responsibilities came under attack. Some married men did the arithmetic and decided that childless married couples were getting an unfairly sweet deal. One suggested that rather than giving husbands who were not yet fathers a tax exemption, the women in childless married couples should be conscripted to work.87 And single professional women and widows wondered why childless couples with two incomes should have a greater part of their joint income exempt, just because they were married. After all, single women had houses and sometimes dependent relatives as well.88

54 Whether as wives, widows, or spinsters, women in the Maritimes along with other Canadians found that the assumptions about families and households that were built into the 1942 wartime income tax statute sometimes fit very awkwardly with the real relationships of cost and contribution in their lives as members of families, kin networks, and communities. In 1942, an editorial writer at the Herald praised Ilsley’s finance department for trying to accommodate these variations: “For the first time in our reading, observation and experience, there is a disposition at Ottawa to consider the peculiar case of the individual taxpayer and to make ‘new types of adjustments’ accordingly.”89 But doing so was fraught with difficulty. By 1944, Ilsley confessed confidentially to a Nova Scotian colleague: “Income tax exemptions of any particular class give the Government more trouble than almost anything else.” Responding to his colleague’s very appealing suggestion for an increased exemption for older war veterans, Ilsley, rather tiredly, pointed out “we are continually considering and trying to deal in an equitable manner with such claims but, as you will appreciate, it will be completely impossible to convert our Income War Tax Act into a mosaic of exemptions of one kind and another.”90 Like Drayton after the First World War, Ilsley felt empowered to talk tough to taxpayers. Claims of personal hardship could always be countered by the argument that if for lack of resources the war should be lost, no one’s life would be worth living.91

55 Still, protest on the part of female taxpayers was not futile, either during the Second World War or in the 30 previous years that have been examined in this article. Women’s voices were among those that helped reverse the badly designed, offensively promoted, and awkwardly administered luxury tax after the First World War. During the interwar years, as entrepreneurs or as collateral victims of illegal booze businesses, women helped to produce the high cost of tax collection that became part of the case for more liberal liquor regulation. At the local level, the link between voting and taxpaying meant that revenue-hungry municipalities were pressured to include “the weaker sex” among those obliged to help “finance the town” and thus, also, to confer on them a vote in municipal business. And, in 1946, one of the widows’ income tax concerns had been addressed by a royal commission, and the federal government had rapidly implemented changes to income tax treatment of estates. Ella Murray might well have been gratified that some women in the Maritimes, and elsewhere in Canada, were taking their citizenship seriously, learning to understand taxes and to protest against those they found unjust. She herself never gave up: as late as 1946, when she was over 80 years of age, she was one of the hundreds of Canadians who wrote to the prime minister to call for the cancellation of the wartime excise tax on soft drinks.92

56 Gender norms and the diverse organization of families are thus implicated in the relations of extraction – that complex web of connections between taxation practices and the various rights and obligations of citizenship. Paying taxes played a part in wage earning, budgeting, saving, supporting dependants, contributing to the nation’s wars, helping to pay unemployment relief, claiming support from the state, preserving class status, and other matters. And in all of these there were particular women’s positions and problems. That no one wants to pay taxes is supposedly a universal truth. But perhaps it is not entirely so. For some women who aspired to full participation in the public affairs of their day, paying their share of taxes was not only a matter of principle, but also a means to gaining full civil rights as voters. Others, who resisted paying, did so not just to save a few dollars from “the government” but to make their entire living by way of tax evasion. They (or sometimes the breadwinners who supported them) used the controversial, increasingly discredited, customs and excise taxes as the means to survive (if precariously). This was hardly good citizenship, but it was a kind of political and economic agency that allowed them to cope in an unfair world that, from their disadvantaged position, they could not change.